Payday Super & Financial Impact: How It Will Change Your Business Cash Flow

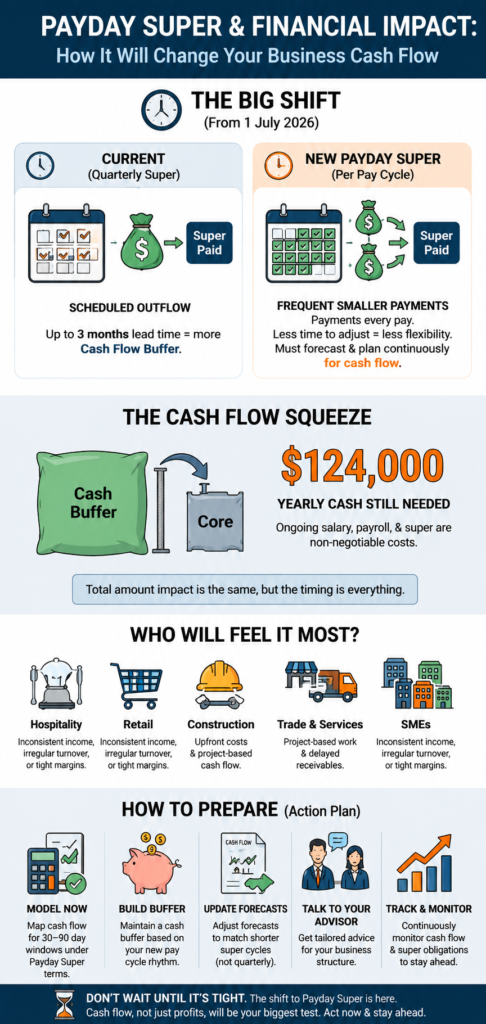

With Payday Super, the shift from quarterly to per-payday obligations means shortfalls.

Payday Super doesn’t just change when you pay super. It also changes how super is calculated. If you’re a small business owner, it’s important to understand these shifts — because they could affect how much you owe and for which employees.

From OTE to Qualifying Earnings

Under the current system, super guarantee is calculated as 12% of an employee’s “ordinary time earnings” (OTE). OTE generally includes base salary, commissions, shift loadings, and some allowances, but excludes overtime.

From 1 July 2026, the calculation shifts to “qualifying earnings” (QE). QE is a broader concept that brings together OTE, salary sacrifice contributions, and certain other amounts that are currently part of an employee’s salary or wages for super guarantee purposes.

For most employees on straightforward pay arrangements, the practical difference may be minimal. But if you have staff on salary sacrifice arrangements, complex pay structures, or variable earnings, QE could change your super liability. It’s worth understanding exactly which payments are now captured.

The Maximum Contribution Base Is Going Annual

Here’s a change that could affect businesses with higher-income employees.

Currently, there’s a maximum super contribution base (MSCB) applied quarterly. If an employee’s earnings exceed the quarterly cap, you’re not obligated to pay SG on the amount above it.

Under Payday Super, the MSCB moves from a quarterly threshold to an indexed annual threshold. This smooths out the calculation across the full year.

Why does this matter? Consider an employee who earns a steady salary but receives a large one-off bonus in one quarter. Under the current system, that bonus might push them over the quarterly cap, meaning you don’t owe super on the excess. Under the annual threshold, that same bonus is spread across the year’s cap. If the employee’s total annual earnings stay below the annual limit, you’ll owe SG on the full amount — including the bonus.

For some businesses, this will mean paying more super for certain employees than they do today. For others, it may simplify things by removing the need to monitor quarterly caps.

Per-Payday Calculations

can accumulate faster and become visible sooner. The ATO will have much more frequent data points to identify non-compliance, and the window for DPN lockdown is tighter.

In plain terms: if your company falls behind on super under the new rules, the personal risk to you as a director escalates more quickly than it did before.

Treasury’s Frank Acknowledgement

It’s worth noting that Treasury has openly acknowledged the reform is likely to trigger an increase in insolvencies. Many businesses have historically used the quarterly super cycle as an informal cash flow tool — holding contributions until the due date to manage short-term liquidity.

That practice is no longer viable under Payday Super. Businesses that can’t fund super with every pay run will need to either restructure their operations or face the consequences. For directors, this means having honest conversations about your company’s financial position — now, not in July.

How to Protect Yourself

• Know your obligations. Understand how the Safe Harbour provisions interact with Payday Super and what you need to do to maintain eligibility.

• Monitor cash flow closely. Build cash flow forecasts that incorporate per-payday super obligations and flag potential shortfalls early.

• Stay current on super payments. Even one missed payment could have consequences. Ensure your payroll and payment systems are automated and reliable.

• Document your decision-making. If your business faces financial difficulty, keeping clear records of your efforts to comply and restructure can support a Safe Harbour defence.

• Get professional advice early. If you’re concerned about your company’s ability to meet Payday Super obligations, speak to your accountant and a restructuring advisor before problems escalate.

This Is Not One to Ignore

Payday Super raises the governance bar for company directors. The stakes are personal, the timelines are tighter, and the consequences of non-compliance are more immediate.

If you’re a director and you’re unsure how these changes affect your legal position, book a time to speak with us.

We can help you understand your obligations, review your company’s readiness, and put a plan in place that protects both your business and you personally.